The previous post discusses how the collapse of the ruble is wreaking havoc on the Russian economy. A big swings in currency exchange rates may impact a country (or a company) negatively. It is certainly the case with the Russian economy as discussed by the previous post. In this post, we examine a few more examples of exchange rates.

The exchange rate is the rate at which a domestic currency can be converted into a foreign currency. Let’s look at the example in the previous post, which is based on the following photo.

This photo was taken around December 3. On that day, if you want to buy US dollars in Moscow, you need to pay 54.3 rubles for a dollar. We would say that the exchange rate is 54.3 rubles per dollar or equivalently $0.0184 per ruble.

At the beginning of 2014, the exchange rate is around 33 rubles per dollar. So the rate of 54.3 rubles per US dollar a 11 months later represents a dramatic swing in exchange rate. Currency exchange rates go up and down all the time. In this case, one US dollar can buy 64.5% more rubles now than a year ago. This is a big price drop in rubles in a short period of time!

This big swing in exchange rates is causing a serious problem in the Russian economy. It now costs a lot more rubles to buy one US dollar (64.5% more). As a result, goods priced in US dollars are much more expensive in Russia than a year ago (assuming the US prices stay the same). For example, Russia imports about 40% of its foods. So the loss of value in rubles really hurts at the grocery store.

Let’s look at another example. Here’s a comparison of the yen-USD exchange rates.

- 105.25 yen = 1 USD (at the start of 2014)

- 121.50 yen = 1 USD (December 2014)

The US dollar is buying more Japanese yens now than almost a year ago. When a unit of money (in this case USD) can buy more of something, that something is becoming cheaper. So the Japanese yen is becoming cheaper, or has been devalued or has depreciated. We can divide 1 by the yen amount and come up with the following exchange rates.

- 1 yen = $0.0095 (at the start of 2014)

- 1 yen = $0.00823 (December 2014)

One yen is buying less US dollars than a year ago. When a unit of money (in this case Japanese yen) is buying less of something, that something is becoming more expensive. So in this case, the US dollar is becoming more expensive in relation to the yen.

The US dollar is getting stronger in this almost one-year period of time. The Japanese yen is getting weaker. But the change is exchange rates is not a dramatic as in the Russian ruble example. It costs 15.4% more yens to buy one US dollar than a year ago. This is a significant price increase, but not as dramatic and as severe as the Russian ruble example.

This example of changes in yen-USD example is beneficial to US importers of Japanese goods. Since Japanese yen is getting cheaper, the same amount of US dollars are buying more Japanese goods, or the same amount of Japanese goods will cost less US dollars to buy (assuming the prices in Japanese goods stay about the same).

___________________________________________________________________

How to read exchange rates

When the value of a currency goes up, it appreciates. When the value of a currency goes down, it depreciates. In the example discussed above, the ruble loses its value against the US dollar (one USD can buy more rubles now). On the other hand, the US dollar gains in value against the Japanese yen (one Japanese yen buys fewer US dollars now). We now describe how to tell whether a currency is losing value or gaining value by looking at the exchange rates. Once the dynamics is grasped, some of the subsequent concepts will be easier to understand.

The reason we go into the trouble of spelling this relationship out is that when a currency is losing value, the exchange rate may actually be a bigger number. Recall that 33 rubles = 1 USD a year ago and 54 rubles = 1 USD now (a year later). So the exchange rate is up when the ruble is losing value. But if you convert the rate to a per ruble rate, the exchange rate is actually down. So thinking that “currency depreciation means exchange rate is down” may cause confusion, not to mention that it may be incorrect.

The key to relating the value of a currency to movement of exchange rates is simple. The idea is this. When a unit of money can buy more of the something, that something is cheaper and thus has lost value. When a unit of money buys less of something, that something is more expensive or has gained in value. The following can further illustrate.

This is the dynamics that we experience in the grocery store. If one dollar bought one pound of apples last week and the same dollar buys two pounds of apples now, we know that apples have become cheaper, or apples have declined in values. Though we don’t usually phrase it in this way with apples, we can also say that apples are losing value against the US dollar. So the above observation will help keep things straight when looking at fluctuations in exchange rates.

As discussed earlier, 33 rubles = 1 USD a year ago and 54.3 rubles = 1 USD now (a year later). So one US dollar can buys more rubles than a year ago. So rubles are cheaper or has lost in value. If we convert the exchange rates to be based on one ruble (1 ruble = $0.03 a year ago and 1 ruble = $0.0184 now), then one ruble will buy less US dollars now than a year ago. This points to the fact that US dollars have become more expensive, or have appreciated. Of course, rubles have depreciated if the US dollar has appreciated.

So there are two ways to look at a change in exchange rates, depending on how the rate is expressed. When the exchange rate of the domestic currency (the ruble in this case) is expressed as the rate of the domestic currency per unit of the referenced currency (USD in this case), a drop in value of the domestic currency means that the exchange rates has increased.

In the Japanese yen example, one USD can buy more yens now than a year ago. So the Japanese yen is becoming cheaper, or is dropping in value. Here, the drop in value in the Japanese yen corresponds with a rise in the exchange rate of yens per USD. With the exchange rates expressed as amounts of USD per yen, we can see that one yen now buys fewer US dollars than a year ago. So US dollars are becoming more expensive or has gained in value. Here, the drop in the value of the Japanese yen corresponds with a falling exchange rate of USD per yen.

To keep things straight, it is a matter of figuring out which currency is cheaper or more expensive by determining which currency can buy more of the other currency. To test out this understanding, one more example. This is the exchange rate between Yuan, one unit of the Chinese currency Renminbi and USD.

Note that one US dollar can now buy a little more Yuan than a year ago. So the Renminbi is getting a litte cheaper and is dropping slightly in value against the dollar. Also note that the drop in value for Renminbi corresponds with a slightly rising exchange rate of Yuan per USD. Now convert the same rates to be USD per Yuan.

Note that one Yuan now buy slightly smaller amount of US dollars. This means that US dollar is becoming a little more expensive. Note that the drop in Renminbi corresponds with a slightly declining exchange rate of USD per Yuan.

To determine whether a currency depreciates or appreciates against a referenced currency, just read the exchange rates to see which currency can now buy more (or less) of the other.

___________________________________________________________________

More about exchange rates

If the domestic currency is cheaper against a foreign currency, then goods that are priced in that foreign currency are more expensive. In the ruble example, imported goods priced in US dollars are more expensive in Russia. So a weaker ruble hurts imports into Russia. On the other hand, goods priced in Rubles will be cheaper in the US. So a weaker ruble helps exports of Russian goods. In general a weaker domestic currency hurts imports and helps exports.

It is interesting to examine the Yuan-USD exchange rates again.

6.8272 Yuan = 1 USD (at the start of 2010)

6.0508 Yuan = 1 USD (at the start of 2014)

6.1523 Yuan = 1 USD (December 2014)

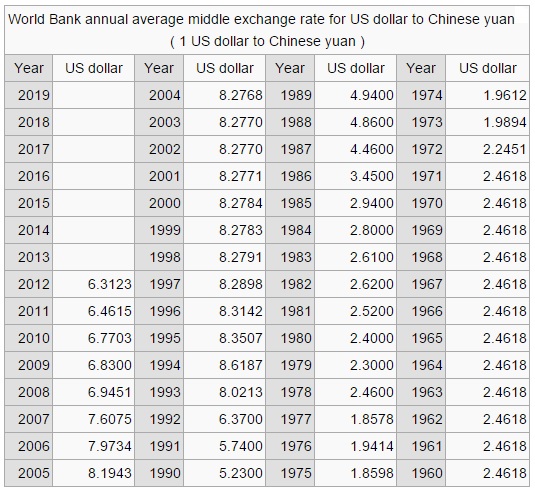

So the larger trend in the last 5 years is that the Chinese Yuan has been rising in value against the USD. From 2010 to the start of 2014, the Yuan had become more expensive (1 USD bought less Yuan at the start of 2014 as compared to 2010). Only in the last year has the yuan been gaining slightly in value against the US dollar. The following is the screen grab of a table in the Wikipedia entry List of renminbi exchange rates.

The exchange rates for Yuan-USD were pretty stable from 1960 all the way to early 1980s. From there the exchange rates for Yuan-USD were on a rising path, which means the Chinese currency had been on a depreciating path. In the early 1980s, one USD could buy around 2.5 Yuans. For the decade 1996-2005, one USD could buy about 8 Yuans. Only in the last decade (2006-2014) had the Chinese currency been gaining in value against the US dollar. Now one USD can buy about 6 Yuans. Many observers believed that the devaluation of the Chinese currency was no accident. Some believed that the Chinese yuan was kept low to promoted exports.

Throughout the period represented in the above table, a US dollar can buy increasingly more and more Yuans. As a result Chinese products are more and more attractive to consumers in the US (from a price perspective). In the 1980s, one USD could buy about 2-5 Yuans. In the 1990s, one USD could buy about 8 Yuans. Set aside the cause of this depreciation of the Yuan, it is undeniable that the weakening of a currency promotes the exports of that country.

___________________________________________________________________

Currency depreciation is good for exports

The statements (1a) and (1b) above are handy device to help keeping things straight. Using them will help decide which currency is becoming cheaper or more expensive. Another handy device is to know that the depreciation of the domestic currency against a foreign currency is good for exports to that foreign country.

Fix a currency and consider it as the base currency (or domestic currency). The base currency is compared against a foreign currency. The following conditions mean the same thing.

- The exchange rate of the number of units of the base currency per unit of a foreign currency is rising.

- The base currency is depreciating against the foreign currency.

- Goods priced in the base currency are cheaper in the foreign country.

- The exchange rate movement present a favorable environment for exports to the foreign country.

Of course, we can also have another set of statements relating currency appreciation and import by flipping the above statements.

One remark that should be made is that the exchange rate mentioned in the above 4 statements is the nominal exchange rate between the base currency and the foreign country. The nominal exchange rate is the number of units of the domestic currency that can purchase a unit of a given foreign currency. It does not take purchasing power into account. For example, when the domestic currency depreciates against a foreign currency, a unit of the foreign currency can now buy more units of the domestic currency. But if the goods priced in the domestic currency have become more expensive, the price appreciation in the domestic currency may cancel out the effect of the domestic currency depreciation. So we assume that the above 4 statements are based on nominal exchange rates.

___________________________________________________________________

Dealer’s buy price and sell price

The above discussion talks about one exchange rate, which is the nominal exchange rate. When you go to foreign currency dealer, there are actually two rates. The dealer buys low and sells high (the dealer has to make a profit). In the above photo, the lower rate is 53.15 rubles per USD and the higher rate is 54.3 rubles per USD. When a tourist walks in that foreign currency store to exchange US dollars into rubles, the tourist will get 53.15 rubles for each US dollar. On the other hand, a Moscow resident who wants to exchange rubles into US dollars will have to pay 54.3 rubles to get a US dollar. The dealer buys low and sells high. The customer sells low and buys high. The spread between the two rates represents the dealer’s profit. The lower rate of 53.15 rubles per USD is called the bid price. That is the price at which a dealer is willing to buy the US dollar. The higher rate of 54.3 rubles per USD is called the ask price (or offer price). That is the price at which a dealer is willing to sell the US dollar.

The same photo also shows the exchange rates for Ruble-Euro. On that day when this photo was taken, any body who wants to sell Euro could only get 65.55 rubles for each Euro. Anyone who wants to buy Euro will have to pay 67.2 rubles for each Euro. The spread between the dealer’s buy price and sell price reflects the balance between demand and supply (or the lack of). If supply and demand are in equilibrium, the spread is likely narrow. If there is more demand for Euro than supply, the spread will be wider.

___________________________________________________________________

Exercises

Consider the following exchange rates.

- KRW-USD (KRW = South Korean Won)

- 1140.50 KRW = 1 USD (at the start of 2013)

- 1150.25 KRW = 1 USD (at the start of 2014)

- 1113.96 KRW = 1 USD (December 2014)

At the start of 2013, a US importer signed a contract with a South Korean electronic maker to buy 1 billion KRW worth of smart phones. The goods were to be delivered one year later and purchase price of 1 billion KRW was also to be paid at the time of delivery. Discuss how the exchange rate movement impacted the transaction. How much more or less had the US importer had to pay in US dollars at the time of delivery as compared to one year earlier?

At the start of 2014, the same US importer signed another contract with the same South Korean electronic maker to buy 1 billion KRW worth of smart phones. The goods were to be delivered 11 months later and purchase price of 1 billion KRW was also to be paid at the time of delivery. Discuss how the exchange rate movement impacted the transaction. How much more or less had the US importer had to pay in US dollars at the time of delivery as compared to 11 months earlier?

___________________________________________________________________

Apples are cheaper

Apples are cheaper